CONFIRMED BY ILL. SUPREME COURT– YOU ARE VIEWING THE MOST DANGEROUS BLOG IN ILLINOIS. This blog warranted a 3 year suspension by the ARDC/Jerome Larkin! Mottos: "Sunlight is the best disinfectant". Justice Louis Brandeis ; "If the truth can destroy something, then it deserves to be destroyed" Carl Sagan; "Justice is Truth in Action" Benjamin Disraeli. Illinois uses the ARDC to quash dissenting attorney activist blogs ; "The freedom of the press is one of the greatest bulwarks of liberty, and can never be restrained but by despotic Governments" — (1776-First Amendment preamble adopted by 8 US colonies)

Former Patent and Trademark Attorney practicing in Chicago, Illinois accepting clients nationwide. We also did trademarks, general intellectual property and business litigation. See our website at www.DenisonLaw.com. Now suspended for 3 years by the Illinois Atty Regn and Disciplinary Commission for blogging about corruption and telling truths that the ARDC wants to cover up. And while I am doing that, I will continue on my blogging work. Now I work full time on court corruption and corruption at the ARDC and JIB (Illinois attorney and judge discipline boards)

Judge Leith was appointed in 2011 in response to concerns about her predecessors being too closely connected to guardianship professionals. Unfortunately, Judge Leith’s actions have also been problematic.

Serious concerns about her actions are documented in a set of 13statements about Judge Leith that the Probate Trap submitted to Colorado Governor Jared Polis and in a detailed judicial ethics complaint filed against her in 2025.

Because adult guardianship records are sealed in Colorado, public information provides only a partial picture of the underlying proceedings. The stories documented in our submission to Governor Polis represent, in all likelihood, only a fraction of the full story.

Summary of the Sykes Financial Elder Abuse Guardianship.

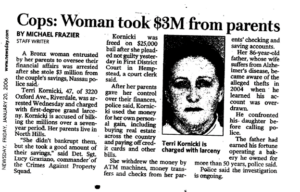

Mary Sykes was a widow (her husband was a Chicago Police officer). She was the mother of two adult daughters. One daughter was a journalist, and the Second was a married suburban matron. Mary was active in her local community and a very vocal member thereof. In particular, her activities in the garden club were legendary – so much so that she was informally listed as a community asset.

The guardianship commenced when Mary discovered that a daughter had removed $2000 from Mary’s savings without permission and became unpleasant about the activity. Mary sought a PROTECTIVE ORDER against the offending daughter.

All of the foregoing occurred in Cook County, Illinois. I mention this because Cook County is unique. Normally, Financial Elder Abuse is a crime – in Cook County certain Judges consider the same to be an opportunity. The provisions of 720 ILCS 5/17 – 56 are a decorative – not to be taken seriously.

My involvement occurred because a group of Mary’s neighbors came amass to consult with me and ascertain how Mary, an elderly lady – well able to fend for her self (and did) was the subject of what they considered to be a predatory guardianship. They reasoned that as Mary knew the objects of her bounty, the extent and nature of her estate, and could (and did) make quite reasonable purchases at the local stores a Guardianship had to be wrongful. They asked me to investigate.

I accepted the assignment and commenced making inquiries. The mere mention of a inquiry outraged the Cook County “powers that be” and a received a telephone call from the attorney for the Court appointed plenary guardian of Mary, and the attorney for the Court appointed Guardian ad litem. They threatened me with dire consequences if further inquiry occurred.

I was not intimidated, and continued inquiry. My inquiry revealed unequivocal FINANCAL ELDER ABUSE and a Judge who appeared to me to not take her oath as Judge very seriously. I reported back to my potential clients.

Before my de facto clients (Mary’s neighbors and friends) could formally engage me, and before I filed document one in the Circuit Court of Cook County the Guardian ad litem and Mary’s guardian filed a Motion for Sanctions against me. I protested and pointed out that I had not appeared in the case – as yet – and had not filed document one. In other words – I was not as yet before the Court.

No problem – as I said this is Cook County, Illinois. I was fined approximately $5000.00! Naturally I appealed to the Appellate Court of Illinois. The Guardian requested and received fees to address the Appeal. Even the Appellate Court could not garner jurisdiction under the above circumstances, but, true to the standards of justice that is in vogue in the Circuit Court of Cook County, Illinois at the time that the Sykes case was being adjudicated the Court reversed the sanction and rendered it for nought – HOWEVER, my indiscretion of objecting to the felonies of 720 ILCS 5/17 – 56 being perpetrated against Mary Sykes the Court recommended that my conduct be evaluated by the ILLINOIS ATTORNEY REGISTRATION AND DISCIPLINARY COMMISSION OF THE SUPREME COURT OF ILLINOIS.

I assume you are aware that all efforts to protect the rights, privileges, and immunities of Mary Sykes and prevent her exploitation in violation of 720 ILCS 5/17 – 56 were in vain. (As it appears such is routinely the situation). Mary’s estate was ravaged and ultimately, she had to die to escape the Guardianship. (I did hear that the United States Department of the Treasury filed a substantial lien against one of guardians – I cannot verify if the tax lien is related to the Sykes litigation). I received a suspension for my discourtesy to the Judges assigned to the Sykes case, and after 53 years in the active practice of law – including but not limited to a bit of recognition in WHOS WHO et al for my achievements – I retired on the threshold of my 80th birthday and the recognition I was old. (I’ll be 90 years of age in July!).

The Sykes case and others similar to it are not to be taken likely. They should be taken seriously. Unfortunately, they are not – they are prime source of corruption and financial elder abuse! The fact that I am not the man I was in my 20’s and I’m as sharp as I was does not mean that I need the assistance of a guardian. Indeed, I am slower than I was in my 20’s and I no longer have a partial photographic memory. Heck – I’m asked by my “peers” to play racquetball today not because of my dexterity or skill, but out of courtesy. Worse yet, in some circles I’m not even invited to play. (If the Judge appointed guardians were in the competition – they would have been excluded 20 years prior – not just recently.

America – and especially Illinois – has laws! Guardianship such as Sykes, Sallas et al are “legal” thievery in the nature of FINANACIAL ELDER ABUSE. The problem is they are very lucrative and easy to conceal – as the judiciary is hand and glove a participant in the felonies. With Judicial orders authorizing every felony theft, including but not limited to Medicaid, and other government frauds, it is difficult to induce public officials, attorneys, and other persons employed to protect the elderly and government institutions to step up and do their jobs – THERE IS NO PRECENTAGE IN IT.

Here in Illinois the Michael Madigan cases stand as a clear caveat – yes, Mike recently went to jail, but, how many years did the whistleblowers receive punishment for “ratting” on the sovereign. How many were punished to a lack of respect for the criminals openly and notoriously allegedly violating 720 ILCS 5/17 – 56. Let me put it another way – how many lawyers do you see are willing to file a case under the act? Is the inducement of triple damages, attorney fees, and a reduced standard of proof an inducement for a lawyer to even investigate Guardianship fraud?

In my prior e-mail I referred you to Attorney JoAnne Denison. Ms Denison is an attorney with alleged technical skills. Mr. Dean Sallas, during the Covid pandemic, opted to attend the guardianship hearings involving his wife by Zoom. Sallas who is year my junior went to Ms. Denison and requested help in making Zoom available to him. His wife’s guardian – the Cook County Public Guardian – and other alleged predators were outraged! How dare Ms. Denison make Zoom available to Mr. Sallas! The reported the ethical breach to the Illinois Attorney Registration and Disciplinary Commission of the Supreme Court of Illinois (IARDC). So outrageous was the offense of providing possible justice of Mr. and Mrs. Sallas that the IARDC) immediately commenced in investigation. A “trial lawyer” was sent to Ms Denison to investigate the insidious event, and a subpoena was dispatched to Goggle to obtain the information on Mr. Sallas’ account.

Ultimately, after a few letters of outrage were dispatched to the IARDC, Attorney Denison received information that the IARDC was not going to investigate further. The long and short of the event was Mr. and Mrs. Sallas retirement estate of approximately 8 million dollars is gone, Ms. Sallas lives in a nursing home, Mr. Sallas lives in his vehicle parked in the parking lot of a church, and their luxury home in Skokie is now owned by the mesne assignee to the ****** Bank.

This has been a slow moving case, which has worked to Pasulka’s benefit. There were a total of 5 cases against Pasulka.

-He beat 1 at a bench trial.

-Another was dismissed for the Statute of Limitations. I blame the ARDC for having knowledge of the criminal act and holding the information until it became public and they had to report it; but by then, it was too late for the State to prosecute.

-We have another one where I am unsure of the Status because the victim passed away recently. It’s a heartbreaking case and personal to many of us. The victim, Aneta, was one of us, one of our advocates. She was also a lawyer who filed a federal lawsuit against her family law judge and GAL to expose the system. What pisses me off is that while Aneta was dying, Pasulka was granted permission to leave the State to go to San Diego for two weeks last month. I do not believe that many people, or the court, knew she was dying, but the fact that the bastard gets to take off for two weeks while victims suffer bother me.

-There are still two active cases open.

Pasulka’s next court date is a Status Date set for August 6, 2025 at 9:00 AM, Court Room 706 at 26th and California. Zoom information is:

Zoom Meeting ID: 957 3244 3804

Zoom Meeting Password: 455947

When you log-in, include “Pasulka observer” in your name so the judge knows to let you in.

I am looking for lawyers, law students and attorneys to help me on this case. I am only a 67 year old mother of 4 and a no body. Most of my complaint was taken from another one professionally prepared by a group of think tank lawyers. Currently, this is what Judge April Perry and I discussed in the Northern District Court for the Eastern Division of federal court this morning, 7/17/25

United States District Court

Northern District of Illinois – CM/ECF NextGen 1.8 (rev. 1.8.3)Notice of Electronic Filing

The following transaction was entered on 7/17/2025 at 11:53 AM CDT and filed on 7/17/2025

Docket Text: MINUTE entry before the Honorable April M. Perry: Status hearing held 7/17/2025. The Court discusses with Plaintiff that, based on the allegations in the current complaint, there is no basis for Article III standing and that the injunctive relief sought by Plaintiff is impossible at this time for the Court to provide. Plaintiff expresses several ideas about how the complaint may be amended to establish both a viable form of relief and standing. While the Court expresses concerns that Plaintiff will be able to state a viable legal claim, she is given until 8/7/2025 to amend the complaint to attempt to do so. Mailed notice. (jcc,)

End docket quote

One of the ways to attain standing is by membership in an organization.

For example, in Monsanto Co. v. Geertson Seed Farms24 the Animal and Plant Health Inspection Service (APHIS), a division of the United States Department of Agriculture, had decided to deregulate a variety of generally engineered alfalfa. The district court held that APHIS violated a federal statute by issuing the deregulation decision without sufficiently assessing the environmental consequences. It vacated APHIS’s deregulation decision, ordered APHIS to prepare an environmental impact statement before deciding the deregulation petition, enjoined planting of the genetically engineered seeds pending APHIS’s completion of the environmental impact statement, and issued related relief. The government and owners of the intellectual-property rights in the seeds appealed, challenging the scope of the relief. The court of appeals affirmed, and the Supreme Court granted review. The respondents who opposed review (conventional seed farms and environmental groups) argued that the government and intellectual-property owners lacked standing to appeal.

The Supreme Court held that the appellants (petitioners in the Supreme Court) did have standing to appeal

you can find a copy of my file stamped complaint here.

it must be amended because so many things have changed since I first filed it.

I am looking for law firms and organizations that can help me with this lawsuit, so if you kow of any, please have them contact me. joanne@justice4every1.com

Legal research on Standing, Article sec 2 so far:

Google AI on standing Article 3, § 2:

Article III of the U.S. Constitution requires that federal courts only hear “Cases” and “Controversies,” which necessitates that a plaintiff have standing to sue. Standing requires demonstrating an injury in fact, causation, and redressability. Leading cases like Lujan v. Defenders of Wildlife, Spokeo, Inc. v. Robins, and TransUnion LLC v. Ramirez have shaped the understanding of these requirements.

Article III Standing Requirements: Injury in Fact: The plaintiff must have suffered or be imminently threatened with a concrete and particularized injury. This injury cannot be hypothetical or a generalized grievance shared by the public.

Causation: The injury must be fairly traceable to the defendant’s conduct. The connection between the injury and the defendant’s actions cannot be too attenuated. Redressability: It must be likely that a favorable court decision will redress the injury. The requested relief must be able to remedy the harm suffered. Key Cases: Lujan v. Defenders of Wildlife (1992): . Established the foundational elements of Article III standing: injury in fact, causation, and redressability. Spokeo, Inc. v. Robins (2016): . Addressed the concreteness of injury, emphasizing that a statutory violation alone is not sufficient for standing; the injury must be concrete and particularized. TransUnion LLC v. Ramirez (2021): . Further clarified the injury in fact requirement, holding that a statutory violation that does not cause a concrete harm does not confer standing. Baker v. Carr (1962): . Established that federal courts could hear cases about state legislative apportionment, a significant step in ensuring equal representation according to SpringerLink. Warth v. Seldin (1975): . Illustrates a situation where plaintiffs lacked standing because they failed to show a direct connection between the challenged zoning ordinances and an injury they suffered according to UMKC Law School. Clapper v. Amnesty International USA (2013): . Dealt with the standard for establishing standing based on future harm. Hollingsworth v. Perry (2013): . Clarified the government’s standing to appeal in cases involving constitutional challenges. DaimlerChrysler Corp. v. Cuno (2006): . Ruled that state taxpayers generally lack standing to challenge state tax or spending in federal court simply by virtue of their taxpayer status. Diamond v. Charles (1986): . Determined that citizens generally need a direct stake in the outcome to challenge a state statute in federal court. Standing to Appeal: To appeal a federal court decision, a party must demonstrate an injury fairly traceable to the judgment below and that a favorable ruling would redress that injury, according to the International Association of Defense Counsel. In essence, Article III standing ensures that federal courts only hear genuine legal disputes, preventing them from being used to resolve abstract grievances or issues of public policy that are best addressed by other branches of government.

The U.S. Supreme Court held that a group of doctors, nurses, and medical associations did not have the right under the U.S. Constitution, a doctrine known as “standing,” to challenge Food and Drug Administration (FDA) regulations governing the use of the abortion drug mifepristone in FDA v. Alliance for Hippocratic Medicine, No. 23-235 (June 13, 2024). This ruling could make it harder for organizations to successfully challenge corporate diversity, equity, and inclusion (DEI) initiatives.

Standing and Why It Matters The concept of standing is fundamental to federal court jurisdiction. Article III § 2 of the U.S. Constitution limits the issues federal courts can resolve to “cases” (lawsuits seeking to protect and enforce rights or to prevent and punish wrongs) and “controversies” (disputes or disagreements between parties). To qualify as a case or controversy, a plaintiff must have a personal stake in the outcome. In the words of Supreme Court Justice Antonin Scalia, to bring a federal lawsuit, a plaintiff must answer the basic question that embodies the concept of standing: “What’s in it for you?”

To establish standing, the plaintiff must demonstrate:

The plaintiff suffered or likely will suffer an injury in fact; The defendant caused or likely will be the cause of the injury; and The requested judicial relief likely will redress the injury. If the plaintiff cannot satisfy all three requirements, the court must dismiss the case for lack of jurisdiction.

Injury In Fact An injury in fact must be a specific and actual harm. A general complaint or harm that may happen is not an injury in fact. As Justice Brett Kavanaugh wrote in Alliance for Hippocratic Medicine, the doctrine of standing “screens out plaintiffs who might have only a general legal, moral, ideological, or policy objection” to a particular action.

In cases involving challenges to DEI initiatives, courts have ruled the plaintiffs failed to demonstrate an injury in fact because they could not show they would have received the benefit sought in the absence of the alleged discrimination. In two cases against the same defendant, White plaintiffs alleged that a grant program available only to Black, Latinx, and Native American applicants was unlawful race discrimination. Courts in both cases ruled that the plaintiffs lacked standing because they failed to show the defendant would have chosen them as grant recipients were it not for their race, making the plaintiffs’ alleged injury too speculative to be an injury in fact. Similarly, the U.S. Court of Appeals for the Sixth Circuit dismissed a case for lack of standing where the plaintiff failed to allege they met the non-race-related requirements for that grant and therefore failed to allege an injury in fact.

In Alliance for Hippocratic Medicine, the Alliance argued the loss of considerable resources spent unsuccessfully opposing the FDA’s regulation constituted an injury in fact. Rejecting this argument, the Court stated, “[A]n organization that has not suffered a concrete injury caused by the defendant’s actions cannot spend its way into standing.”

Causation Once a plaintiff has shown an injury in fact, the plaintiff must establish a chain of events leading from the defendant’s actions to the asserted injury. The Court’s analysis of causation in Alliance for Hippocratic Medicine is instructive. The Alliance alleged that the FDA’s rule would injure a doctor’s conscience by forcing the doctor to provide a life-saving abortion to someone experiencing complications from taking the drug mifepristone. The Court emphasized federal statutes expressly and definitively protect doctors from providing medical care that violates their consciences. These statutes break the chain of events that would connect the FDA’s rule authorizing the use of mifepristone to the alleged injury and thus defeat the plaintiff’s attempt to show causation.

Redressability The third prong of the standing test is whether a court can redress, or cure, a claimed injury. Redressability and causation are closely related. If the defendant did not cause the injury, then the court cannot redress the injury by any order to the defendant. Even if the plaintiff plausibly alleges causation, redressability may depend on the nature of the relief requested.

For example, the U.S. Court of Appeals for the Tenth Circuit found a plaintiff challenging an employer’s mandatory DEI training lacked standing because he could not demonstrate redressability. The plaintiff alleged that the defendant’s mandatory DEI trainings caused him to suffer the injury in fact of a hostile work environment. The plaintiff sought an injunction prohibiting the defendant from using or distributing DEI materials. However, because the plaintiff had resigned from his employment by the time he filed the lawsuit, the court held that a change in the defendant’s policy would not redress any ongoing injury to the plaintiff.

Associational Standing The Supreme Court has long recognized that, in appropriate circumstances, organizations may have standing to pursue claims on behalf of their members. This is known as “associational,” “organizational,” or “third party” standing and is a heavily litigated issue in organizations’ lawsuits challenging DEI programs and practices.

To prove associational standing, the plaintiff organization must demonstrate:

The organization’s members would have standing in their own right; The interests the association seeks to vindicate are germane to the association’s mission; and Neither the claim nor the relief requested requires the participation of the individual members. Whether establishing standing requires an organization to identify members by name depends on where the plaintiff filed the lawsuit. The Eleventh Circuit held in a 2-1 decision that an organization had standing to sue even though it declined to identify by name any member that suffered an injury in fact. (The dissenting judge observed that the organization offered no good reason for withholding members’ names and suggested that the anonymous members suffered no injury in fact but were merely lending their identities for the purpose of the litigation.)

The Second Circuit came to the opposite conclusion, dismissing an organization’s challenge to a fellowship program for lack of standing because the plaintiff organization refused to name even a single member who had suffered harm. The First Circuit also has held that a plaintiff organization must name an injured individual to support associational standing. The U.S. Supreme Court likely will have to resolve this split in the circuits.

Takeaways for Employers The first line of defense for employers facing legal challenges to DEI practices is to evaluate whether the plaintiff has the right to bring the case at all. Although standing arguments are fact specific, employers can ensure those who challenge private sector DEI programs have a demonstrable connection to such programs. A successful defense based on an individual or organization’s standing allows employers to evaluate and, if necessary, modify DEI programs to withstand legal challenges.

Jackson Lewis attorneys are available to answer your DEI questions and help you ensure your DEI programs are carefully designed, documented, and implemented to comply with applicable law.

Focused on employment and labor law since 1958, Jackson Lewis P.C.’s 1,000+ attorneys located in major cities nationwide consistently identify and respond to new ways workplace law intersects business. We help employers develop proactive strategies, strong policies and business-oriented solutions to cultivate high-functioning workforces that are engaged and stable, and share our clients’ goals to emphasize belonging and respect for the contributions of every employee. For more information, visit https://www.jacksonlewis.com.

Federal-court practitioners will likely have heard of the “irreducible minimum”1 of standing, which Article III of the United States Constitution requires of every plaintiff on every claim: the party invoking the court’s jurisdiction must have an actual or imminent, personalized, concrete injury; the injury must be traceable to the conduct complained of in the lawsuit; and there must be a reasonable probability that a favorable court ruling would redress the injury. Lack of Article III standing is a silver bullet: it is jurisdictional, it cannot be waived, the court must notice a standing defect even if no party raises it, and the appellant’s lack of standing requires dismissal.

Less well known is that an appellant in federal court – whether plaintiff or defendant – must separately have standing to appeal. Standing can present a fatal obstacle to appeals of interest to business lawyers, including class-action settlements, bankruptcies, challenges to government action, cases involving intervenors, and even occasionally appeals from jury verdicts. Understanding appellate-standing requirements can help you stop an adversary’s appeal cold and can keep you from spending time and money on your own client’s appeal that cannot succeed. This article examines the obscure-but-useful area of standing to appeal, highlighting recurring scenarios where parties do or don’t have standing and the considerations at play.

I. Article III Standing

A. Basic Requirements for Article III Standing

Article III of the United States Constitution limits the federal judicial power to “Cases” and “Controversies.”2 To reach the merits of a case, an Article III court must have jurisdiction. “One essential aspect of this requirement is that any person invoking the power of a federal court must demonstrate standing to do so.”3 To establish Article III standing, the party invoking a federal court’s jurisdiction must establish (1) that he or she has actually suffered, or imminently will suffer, a concrete and particularized “injury in fact;” (2) that the injury is fairly traceable to the defendant’s conduct; and (3) that it is “‘likely,’ as opposed to merely ‘speculative,’ that the injury will be ‘redressed by a favorable decision.’”4 The Supreme Court has described these three requirements as the “irreducible minimum” of Article III standing.5

These requirements serve several purposes. They help assure that legal questions will be resolved in a “concrete factual context conducive to a realistic appreciation of the consequences of judicial action.”6 They additionally are meant to ensure that the party invoking the federal court’s jurisdiction has a “‘personal stake’ in the outcome of the controversy” and that the dispute “touches upon the ‘legal relations of parties having adverse legal interests.’”7 They are also meant to keep federal courts within their lane, restraining them from reaching out to decide issues committed to other branches of government.8

These rules also have their own important glosses. A party must demonstrate standing for each claim they press and each form of relief they seek.9 The party claiming standing must show that he “personally would benefit in a tangible way from the court’s intervention.”10 Because the injury must be concrete and personalized, the desire to vindicate “value interests,” “psychic satisfaction,” and the desire to see that “laws are faithfully enforced” cannot support Article III standing.11 Only the party invoking the court’s jurisdiction (normally the plaintiff in the trial court or the appellant in an appellate court) must have standing; the party objecting to relief against itself (normally the defendant or appellee) need not.12

Article III standing is essential to a federal court’s subject-matter jurisdiction.13 Since federal courts are presumed not to have jurisdiction until it is affirmatively shown,14 the record must contain facts affirmatively establishing standing, appropriate to the stage of the litigation.15 If the plaintiff fails to demonstrate standing, the court must usually dismiss the case.16 As with other subject-matter jurisdiction requirements, the absence of standing cannot be waived or forfeited17 and a court must notice a standing defect sua sponte even if no party raises it.18

Article III standing should not be confused with “prudential” standing, a set of principles that formerly limited which plaintiffs could sue even if they had standing in the constitutional sense. The Supreme Court eventually clarified that “prudential standing” was a misnomer. It untangled the prudential-standing doctrine into multiple strands, most of which are irrelevant here.19 When this article speaks of standing, it means Article III standing unless otherwise specified.

B. Article III Standing Applied to Appeals

“Although rulings on standing often turn on a plaintiff’s stake in initially filing suit, ‘Article III demands that an ‘actual controversy’ persist throughout all stages of litigation.’”20 Thus “[t]he requirement of standing ‘must be met by persons seeking appellate review, just as it must be met by persons appearing in courts of first instance.’”21 An appellant–or petitioner in the Supreme Court–must satisfy Lujan’s three requirements, tailored to initiating an appeal rather than filing an initial lawsuit. The test for standing looks to injury to the appellant caused by the lower court’s judgment instead of injury to the plaintiff caused by the defendant’s conduct. “To show standing under Article III, an appealing litigant must demonstrate that it has suffered an actual or imminent injury that is ‘fairly traceable’ to the judgment below and that could be ‘redress[ed] by a favorable ruling’” from the appellate court.22 If the appellant lacks standing to appeal, the court must dismiss the appeal.23

For example, in Monsanto Co. v. Geertson Seed Farms24 the Animal and Plant Health Inspection Service (APHIS), a division of the United States Department of Agriculture, had decided to deregulate a variety of generally engineered alfalfa. The district court held that APHIS violated a federal statute by issuing the deregulation decision without sufficiently assessing the environmental consequences. It vacated APHIS’s deregulation decision, ordered APHIS to prepare an environmental impact statement before deciding the deregulation petition, enjoined planting of the genetically engineered seeds pending APHIS’s completion of the environmental impact statement, and issued related relief. The government and owners of the intellectual-property rights in the seeds appealed, challenging the scope of the relief. The court of appeals affirmed, and the Supreme Court granted review. The respondents who opposed review (conventional seed farms and environmental groups) argued that the government and intellectual-property owners lacked standing to appeal.

The Supreme Court held that the appellants (petitioners in the Supreme Court) did have standing to appeal. Its decision illustrates how the standing requirements apply to appeals as well as some of the intricacies in evaluating standing. The Court started with the bottom line: “Petitioners are injured by their inability to sell or license [the genetically modified seeds] to prospective customers until such time as APHIS completes the required EIS. Because that injury is caused by the very remedial order that petitioners challenge on appeal, it would be redressed by a favorable ruling from this Court.”25

The respondents’ counter-arguments, which the Supreme Court rejected on the facts, also help illustrate how the traditional standing requirements translate to appeal. The respondents contended that the petitioners lacked standing to appeal because their inability to sell or license the seed was caused by a part of the injunction that petitioners did not challenge, namely the district court’s setting aside of APHIS’s deregulation decision. Thus, the argument apparently went, a favorable ruling on appeal would not redress the injury caused by the district court’s judgment (the third Lujan requirement) because even a favorable ruling would not remedy petitioners’ injury (their inability to sell or license the seed). The Supreme Court rejected the argument because the petitioners had always contended that their own proposed judgment should be entered, and that judgment would have allowed planting, and thus sales, of the seed. Additionally, the Court held, the judgment prevented even partial deregulation of the seed without an environmental impact statement, and the appellants were harmed by the preclusion of even partial deregulation. To the respondents’ argument that the injury from precluding partial deregulation was not “actual or imminent” (the first Lujan requirement) because APHIS might not partially deregulate even if allowed to, the Supreme Court explained that APHIS’ litigation conduct showed that there was “more than a strong likelihood that APHIS would partially deregulate [the seed] were it not for the District Court’s injunction.”26

Even a party that seeks United States Supreme Court review of a state-court decision must meet these standing requirements – and can obtain review even if the state-court suit did not satisfy Article III. In ASARCO, Inc. v. Kadish,27 plaintiffs brought a state-court suit against an Arizona land agency, seeking a declaration that a state statute governing mineral leases on state lands was void under both federal law and the state Constitution. Mineral lessees of state school lands intervened as defendants. The trial court upheld the statute, but the Arizona Supreme Court reversed and held the state statute invalid as applied to certain mineral leases. The U.S. Supreme Court granted the mineral lessees’ petition for certiorari. It explained that while the original plaintiffs did not have a sufficient injury to have Article III standing to bring suit in federal court, state courts were free to entertain suits that federal courts cannot. The parties seeking to invoke the jurisdiction of a federal court – the United States Supreme Court – were defendants that had lost in the Arizona Supreme Court: leaseholders who had been granted leases under the law and procedures held invalid by the Arizona Supreme Court.28 They had Article III standing to seek Supreme Court review because they were injured by the Arizona Supreme Court’s judgment. The state supreme court’s decision “poses a serious and immediate threat to the continuing validity of those leases by virtue of its holding that they were granted under improper procedures and an invalid law.”29 If the United States Supreme Court agreed with petitioners’ legal argument, it would reverse the Arizona court’s decision and remove the decision’s disabling effect on the petitioners. Thus, the petitioners “first invoking the authority of the federal courts” had met all of the Article III standing requirements: the state courts’ adverse adjudication of their legal rights was “the kind of injury cognizable in this Court on review from the state courts.” They had personally suffered actual or threatened injury as a result of the putatively illegal conduct. The injury could fairly be traced to the challenged action, and the injury was likely to be redressed by a favorable decision.30 “When a state court has issued a judgment in a case where plaintiffs in the original action had no standing to sue under the principles governing the federal courts, we may exercise our jurisdiction on certiorari if the judgment of the state court causes direct, specific, and concrete injury to the parties who petition for our review, where the requisites of a case or controversy are also met.”31

An intervenor can also have standing to appeal, if it meets the Article III requirements. In Food Marketing Institute v. Argus Leader Media,32 the district court compelled the United States Department of Agriculture to disclose certain data about grocery stores under the Freedom of Information Act. The USDA declined to appeal, but the Food Marketing Institute (a trade association of grocery stores) intervened and appealed. The court of appeals affirmed, and the Supreme Court granted review. Discussing whether the Institute had Article III standing to appeal, the Supreme Court explained that the disclosure ordered by the trial court “likely would cause [the association’s members] some financial injury” because the grocery-store industry was highly competitive and disclosure of store-level SNAP data would help competitors win business from the Institute’s members.33 Further, this “concrete injury is … directly traceable to the judgment ordering disclosure,” and a “favorable ruling from this Court would redress the retailers’ injury by reversing the judgment.”34

C. Distinction Between Standing to Sue and Standing to Appeal

An appellant’s standing to appeal is different from the plaintiff’s standing to file the lawsuit in the first place. While an appellate court is obligated to satisfy itself that jurisdiction, and thus standing, existed in the lower court as well as in the appellate court,35 they are separate inquiries.

For example, a party that did not even have Article III standing in the trial court may still be injured by the judgment and have Article III standing to appeal. In Seila Law LLC v. Consumer Financial Protection Bureau,36 the Consumer Financial Protection Bureau had issued a civil investigative demand to a law firm, Seila Law LLC. The CFPB petitioned the district court to enforce the demand. Seila opposed the petition, contending that the CFPB’s leadership structure violated the United States Constitution because the President could only remove the agency’s director for cause. The district court enforced the demand, and the court of appeals affirmed. The Supreme Court granted Seila’s petition for review, and an amicus argued that Seila lacked standing to appeal because the demand would have been issued even in the absence of the CFPB director’s removal protection. The Supreme Court held that the argument did not defeat the district court’s jurisdiction. Seila, it explained, “is the defendant and did not invoke the [District] Court’s jurisdiction,” and “[w]hen the plaintiff has standing, ‘Article III does not restrict the opposing party’s ability to object to relief being sought at its expense.’”37 The Court continued that Seila’s “appellate standing is beyond dispute” because it had been “compelled to comply with the civil investigative demand and to provide documents it would prefer to withhold,” that “injury is traceable to the decision below and would be fully redressed if we were to reverse the judgment of the Court of Appeals ….”38

In ASARCO, Inc. v. Kadish,39 a party injured by a state-court decision on a question of federal law obtained United States Supreme Court review, even though there would not have been standing to bring the action in federal court to begin with. By adjusting legal relations, the state court’s judgment can cause the losing party an Article III injury even if there would not previously have been an injury sufficient to support standing.40

II. How Article III Standing Can Make or Break an Appeal

Even where a client is upset enough about a trial judge’s ruling to spend the time and expense to appeal, Article III standing can block the appeal unless a favorable ruling from the appellate court will concretely and personally benefit the client. The issue most often arises in cases seeking injunctive or declaratory relief rather than money, but it can occasionally arise on appeal from a damages judgment as well. To illustrate, we walk through some recurring (and overlapping) scenarios where appeals have been dismissed for lack of standing, then examples where the courts upheld standing even though on the surface the appellant appeared to lack the required personal stake in the outcome. These scenarios are not exhaustive, but they illustrate the considerations involved and should be of the most interest to business lawyers.

A. Example Situations Where Appeals are Dismissed for Lack of Standing

Appellants Challenge Aspects of the Judgment That Do Not Adversely Affect Them

If the appellant was not injured by the challenged aspect of the lower court’s judgment, or an appellate decision could not effectively redress that injury, the appellant lacks Article III standing to appeal.

In Waid v. Snyder (In re Flint Water Cases),41 appellants objected to a provision in a class-action settlement. They objected to a provision in the district court’s decision awarding 17% of their recovery to lead class counsel and 8% to their independently retained counsel. But, if that provision were struck down, those appellants would instead pay 25% of their recovery to lead class counsel. Either way, they would pay 25% in common benefit awards and fees. “[B]ecause [these] Objectors would fare no better with or without the Common Benefit Assessments applicable to their claims, they fail to demonstrate that they have suffered an injury in fact. Accordingly, [these] Objectors lack standing to appeal the Common Benefit Assessments” at issue.42 They also could not challenge common benefit fund assessments associated with child plaintiffs, because the objectors were adults and would not be affected by any change to the common-benefit fund related to minors.43

An appellant similarly lacks Article III standing to appeal a ruling that only harms someone else. In Kimberly Regenesis, LLC v. Lee County,44 the plaintiff noticed the deposition of a county commissioner in a disability-discrimination case. The county moved for a protective order, arguing that the commissioner had quasi-judicial immunity from discovery, but the commissioner did not. When the district denied the protective-order motion, the county appealed. The Eleventh Circuit held that the county lacked Article III standing to appeal because any immunity belonged solely to the commissioner, not the county, so the county was not adversely affected by the order.45

The Original Party Does Not Appeal, An Intervenor Does Appeal, But the Intervenor Lacks Independent Standing

Diamond v. Charles46 and Hollingsworth v. Perry47 each illustrate how the appellant must personally stand to obtain a concrete benefit from a favorable appellate ruling – and the corollary that when only an intervenor appeals, the intervenor must personally stand to gain a concrete benefit. In Diamond, plaintiffs, challenging the constitutionality of an Illinois law restricting abortion, sued state officials charged with enforcing it. The would-be appellant, pediatrician Eugene Diamond, intervened as a defendant supporting the law. The district court enjoined enforcement of certain provisions but not others; all parties appealed; and the court of appeals affirmed and expanded the injunction. Diamond appealed to the Supreme Court, but the state did not.

The Supreme Court held that Diamond lacked Article III standing to prosecute the appeal. To continue the suit in the absence of the defendant state, Diamond, himself, had to satisfy Article III.48 None of the benefits he hoped to achieve through a favorable ruling, the Court explained, satisfied Article III. If the Court held the Illinois law constitutional, Diamond could not compel the state to enforce the law. A private citizen lacks a cognizable interest in the prosecution of someone else.49 Nor did he have a concrete interest on the theory that a law banning abortion would yield more live births and, eventually, more patients for him as a pediatrician. That benefit was speculative.50 His desire, as a doctor, to litigate the standards that should apply to physicians practicing abortion did not suffice, because “Article III requires more than a desire to vindicate value interests.”51 In short, “Diamond has an interest, but no direct stake, in the abortion process” and his “abstract concern … does not substitute for the concrete injury required by Art. III.”52

In Hollingsworth v. Perry,53 California state voters had passed a ballot initiative amending the state constitution to preclude same-sex marriage. Plaintiffs, same-sex couples who wanted to marry, sued in federal court, contending the state constitutional amendment violated the Due Process and Equal Protection Clauses of the Fourteenth Amendment. They named as defendants California’s governor and other state and local officials charged with enforcing California’s marriage laws. The officials refused to defend the law, so the district court allowed the initiative’s proponents to intervene to defend it. After trial, the district court declared the amendment unconstitutional and enjoined the public officials named as defendants from enforcing it. Those officials did not appeal, but the intervening initiative proponents did. The California Supreme Court meanwhile held that official proponents of a ballot initiative have authority under state law to assert the state’s interest in defending the constitutionality of the initiative when public officials refuse to do so. The court of appeals held that the intervenors had standing to defend the law and affirmed the district court’s order on the merits.

The Supreme Court reversed, holding that the intervening proponents did not have Article III standing to appeal. The Court reiterated that standing “must be met by persons seeking appellate review, just as it must be met by persons appearing in courts of first instance.”54 It explained that plaintiffs had standing to file the case in the district court, against the officials responsible for enforcing the state constitutional amendment. But once the district court issued its order, the Court held, the plaintiffs no longer had any injury to redress. The state officials had not appealed. The “only individuals who sought to appeal” were the ballot proponents. But they had not been ordered to do or refrain from doing anything. Their only interest was to vindicate the validity of a generally-applicable California law. Under settled law, the Court continued, such a “generalized grievance,” no matter how sincere, is insufficient to confer Article III standing.55 The intervenors had no “personal stake” in defending the law that was distinguishable from the general interest of every California citizen, which was not a “particularized interest” sufficient to create a case or controversy under Article III.56 Even though the California Supreme Court had held that the initiative proponents could assert the state’s interest, “standing in federal court is a question of federal law, not state law. And no matter its reasons, the fact that a State thinks a private party should have standing to seek relief for a generalized grievance cannot override our settled law to the contrary.”57

The Appellant’s Only Remaining Interest is Overturning an Attorney-Fee Award

Diamond and Lewis v. Continental Bank Corp.58 also illustrate that wanting to overturn an attorney-fee award is not enough to confer standing to appeal the underlying substantive decision.

In Diamond, the Court held that petitioner Diamond did not have standing on the merits, as already discussed. The Court then held that Diamond did not have Article III standing to appeal on the ground that a successful appeal would overturn the attorney-fee award against him. The district court had ordered him, as a losing defendant, to pay attorney fees of the prevailing plaintiffs. That award would be overturned if the Supreme Court reinstated the law on appeal. The Supreme Court held that even this concrete, direct pecuniary interest in the outcome of the appeal did not provide Article III standing. Standing, the Court held, “requires an injury with a nexus to the substantive character of the statute or regulation at issue” but the “fee award … bears no relation to the statute whose constitutionality is at issue here…. [T]he mere fact that continued adjudication would provide a remedy for an injury that is only a byproduct of the suit itself does not mean that the injury is cognizable under Art. III.”59

Lewis similarly holds that an interest in attorney fees is not enough to satisfy Article III. Continental Bank, an Illinois bank holding company, applied to Florida to establish and operate an industrial savings bank. The Florida state controller, Lewis, refused to process the application because two state statutes prohibited out-of-state holding companies from operating industrial savings banks. Continental sued Lewis in federal court, claiming Florida’s statutes violated the Commerce Clause of the United States Constitution. The district court agreed with Continental and ordered Lewis to process the application. Lewis appealed, and the court of appeals affirmed. But while the appeal was pending, Congress changed the governing federal statute so that it now authorized states to prohibit out-of-state ownership of the kind of bank Continental wanted to open. The Supreme Court held the Commerce Clause challenge moot because Florida’s statutes were now authorized by a federal statute.60 And just as Diamond had held that an interest in overturning an attorney-fee award was not enough to confer Article III standing, the Court held that Continental’s interest in preserving its attorney-fee award as a prevailing party also did not keep the case alive. The “interest in attorney’s fees is, of course, insufficient to create an Article III case or controversy where none exists on the merits of the underlying claim.”61

These holdings articulating that Article III is not satisfied by a litigant’s interest in an attorney-fee award are hard to reconcile with the Court’s classic and still-good-law holding that a class representative does have a sufficient Article III stake to appeal denial of class certification at the end of the case, even though the class representative’s own claim has been adjudicated. The Court held that the class representative’s interest in shifting attorney fees to absent class members, by obtaining class certification, was a sufficient stake to satisfy Article III.62 It is difficult to understand why a plaintiff’s interest in obtaining attorney fees from a defendant, or a defendant’s interest in overturning an attorney-fee award against itself, is insufficient, but a plaintiff’s interest in forcing other plaintiffs to bear some of the attorney fees is sufficient.

The Appellant’s Personal Stake Disappears During the Litigation

Sometimes the plaintiff’s personal stake, which conferred Article III standing at the commencement of the litigation, disappears during the litigation or on appeal. But “[t]he ‘case-or-controversy requirement subsists through all stages of federal judicial proceedings, trial and appellate.’”63 As such, the Supreme Court has consistently held that there is no longer an Article III case or controversy when the appellant’s personal stake disappears during an appeal.

Wittman v. Personhuballah64 illustrates this holding. After the Commonwealth of Virginia adopted new congressional districts to reflect the results of the 2010 census, voters in one of the affected districts sued, claiming the redrawing of their district’s lines was an unconstitutional racial gerrymander. Members of Congress from several Virginia districts intervened to defend the redistricting. A three-judge district court agreed with the voters and set a deadline for the Virginia Legislature to adopt a new redistricting plan. The Commonwealth of Virginia did not appeal, but the intervening members of Congress did. The only parties seeking to defend the redistricting plan, and seeking review of the district court’s conclusion that it was unconstitutional, were the intervening members of Congress. While the appeal was pending, the Virginia Legislature failed to meet the district court’s redistricting deadline, so a special master appointed by the district court developed a new districting plan. The Supreme Court held that because of events during the litigation, “the intervenors now lack standing to pursue the appeal.”65

One of the three members of Congress claiming standing was Representative Randy Forbes, the incumbent in District 4. He had maintained that unless the legislature’s plan was upheld, his district would be transformed from a 48% Democratic district into a safe 60% Democratic district, harming his reelection chances there. As a result, he said, he was running in District 2 instead. He had maintained that the Supreme Court’s decision would make a concrete difference. He would run in District 2 under the current plan, but District 4 if the legislature’s plan were reinstated. His attorney ultimately informed the Court that Forbes would seek election in District 2 regardless of whether the legislature’s plan were reinstated. The Court held that given this letter, “we do not see how any injury that Forbes might have suffered ‘is likely to be redressed by a favorable judicial decision.’”66 Redressability is an essential element of standing, as detailed above. The Court explained that it “need not decide whether, at the time he first intervened, Representative Forbes possessed standing. Regardless, he does not possess standing now.”67

Still, the two other appealing members of Congress – representing Districts 1 and 7 – claimed they had standing to challenge the district court’s order because, unless the legislature’s plan were reinstated, a portion of their electorate would be replaced with voters unfavorable to them, reducing their likelihood of winning reelection. The Supreme Court rejected this argument because the record contained no evidence supporting it. The Court explained that “‘the party invoking federal jurisdiction bears the burden of establishing’ that he has suffered an injury by submitting ‘affidavit[s] or other evidence.’”68 When challenged by a court or opposing party concerned about standing, “the party invoking the court’s jurisdiction cannot simply allege a nonobvious harm, without more.”69 The representatives claimed that unless the legislature’s plan were reinstated, “their districts will be flooded with Democratic voters and their chances of reelection will accordingly be reduced,” but they “have not identified record evidence establishing their alleged harm.”70 Given the holdings about the three representatives, “we conclude that none of the intervenors has standing to bring an appeal in this case. We consequently lack jurisdiction and therefore dismiss this appeal.”71

Trump v. New York72 also treated the disappearance of the plaintiff’s personal stake as a lack of standing to appeal. Trump concerned the decennial census of population in the United States. The President had issued a memorandum announcing a policy of excluding aliens who were not lawfully in the country from the decennial census. The memorandum directed the Secretary of Commerce to report, to the extent possible, not only the tabulation of population, but information permitting the President to carry out the new policy. Several plaintiffs, including the State of New York, challenged the memorandum. The district court held that the plaintiffs had Article III standing because the memorandum was chilling aliens and their families from responding to the census, degrading the quality of census data used to allocate federal funds and forcing plaintiffs to spend resources to combat the chilling effect. The district court enjoined the Secretary from reporting the newly requested information. The government appealed to the Supreme Court.

The Supreme Court held that the appeal no longer presented an Article III case or controversy. The chilling effect that had supported standing in the district court no longer existed, because the census response period had ended.73 The threatened impact of an unlawful apportionment on congressional representation and federal funding did not suffice, because it was not yet clear whether or how the President’s policy would be implemented or what effect it would have on apportionment.74 The Supreme Court concluded that under the current facts, the plaintiffs lacked Article III standing, and the case was not ripe.75

The Appellant Obtained All its Requested Relief in the Trial Court, But Wants Review of Alternative Grounds or Unfavorable Findings

Though not technically grounded in Article III, a closely-related doctrine normally precludes appeal unless the appellant is “aggrieved” by the judgment or order being appealed. A party that received all the relief it requested in the trial court normally cannot appeal because the relief was granted on one ground rather than another,76 or to review unfavorable findings unnecessary to the judgment.77 “Ordinarily, only a party aggrieved by a judgment or order of a district court may exercise the statutory right to appeal therefrom. A party who receives all that he has sought generally is not aggrieved by the judgment affording the relief and cannot appeal from it.”78 The “rule is one of federal appellate practice, however, derived from the statutes granting appellate jurisdiction and the historic practices of the appellate courts; it does not have its source in the jurisdictional limitations of Art. III.”79 So “[i]n an appropriate case, appeal may be permitted from an adverse ruling collateral to the judgment on the merits at the behest of the party who has prevailed on the merits, so long as that party retains a stake in the appeal satisfying the requirements of Art. III.”80

The prudential “aggrieved” requirement may be ripe for reappraisal. The most-commonly-used appeal statutes do not say the appellant must be aggrieved. The Supreme Court’s 2014 decision in Lexmark International v. Static Control Components, Inc. suggests that courts should not apply “prudential” doctrines to conclude that parties lack standing, but should decide non-constitutional standing issues as a matter of statutory interpretation.81 A judge-made “aggrieved” requirement that limits who can appeal, but is not found in the Constitution or statute, is arguably in tension with Lexmark.82 Several lower federal appellate courts have grappled with how Lexmark applies to the judge-made “person-aggrieved” limitation in bankruptcy appeals. Though sometimes changing terminology in response to Lexmark, they have continued to apply the person-aggrieved requirement.83

The Appellant’s Interest is in Advancing Values or Vindicating The Rule of Law

The personal stake required by Article III must be concrete, and the issue must particularly affect the party invoking federal-court jurisdiction.84 Consequently, one cannot appeal to vindicate value interests,85 the rule of law, or to obtain psychological satisfaction.

The Supreme Court’s decision in Hollingsworth v. Perry86 illustrates this principle. As discussed above, state voters passed a ballot initiative amending the state constitution to define marriage as a union between a man and a woman. The district court held the amendment unconstitutional and enjoined the defendant officials from enforcing it. The proponents appealed, but the state officials did not. The Ninth Circuit affirmed the district court’s order. The Supreme Court reversed, concluding that the proponents did not have standing to appeal. Whereas a “litigant must seek relief for an injury that affects him in a ‘personal and individual way,’” and “possess a ‘direct stake in the outcome of the case,’” the proponents had no “‘direct stake’ in the outcome of their appeal.”87 “Their only interest in having the District Court order reversed was to vindicate the constitutional validity of a generally applicable California law” – and such a “generalized grievance,” held in common with the public at large, is “insufficient to confer standing.”88 Vindication of “value interests,” the Court repeated, is “not a ‘particularized’ interest sufficient to create a case or controversy under Article III.”89

Carl F. Schier PLC v. Nathan (In re Capital Contracting Co.)90 illustrates many of the limits on Article III standing to appeal. The facts are complicated, but the Article III holding is simple. The would-be appellant, Carl F. Schier LLP, was a law firm. It had represented the bankruptcy debtor, Capital Contracting, in a state-court lawsuit. Capital Contracting filed bankruptcy, and in the bankruptcy proceedings, Schier filed a claim for legal fees. The bankruptcy trustee then countersued Schier, claiming Schier had committed malpractice in the state court. They settled, and Schier withdrew its fee claim. When the bankruptcy trustee filed a final report, Schier objected that the appeal in the state-court litigation was a valuable asset of the bankruptcy estate that the trustee had failed to administer or abandon. The bankruptcy judge overruled the objection and approved the report, and Schier appealed to the district court. The district court dismissed the appeal, and Schier appealed to the Sixth Circuit.

The Sixth Circuit held that Schier lacked Article III standing to appeal to the district court.91 It recited that to establish injury in fact under Article III, the plaintiff must show an invasion of a legally protected interest that is concrete and particularized and actual or imminent, not conjectural or hypothetical. On appeal, the focus shifts to injury caused to the appellant by the judgment, rather than caused to the plaintiff by the underlying facts.92 The court concluded that “Schier has not shown that it suffered an Article III injury from the bankruptcy court’s order approving the trustee’s final report” despite the report’s failure to list as an asset the right to appeal in the state-court lawsuit.93 “[T]he failure to list those rights could not financially harm Schier” because Schier had settled with the trustee and withdrawn its attorney fee claim.94 Even if a state-court appeal would reduce the state-court judgment against Capital Contracting to zero (and, in the process, vindicate Schier’s position that it had not committed malpractice), “that reversal could not provide Schier with one cent more in attorney’s fees,” since it had withdrawn its fee claim.95 The bankruptcy court’s order did not affect Schier in a “personal and individual way.”96 Schier’s “strong feelings … over the validity of its proposed appeal” did not provide standing, because “Article III courts are not the place for ‘concerned bystanders’ to vindicate ‘value interests.’”97 Schier could not gain standing by saying the trustee and bankruptcy court were required to fix the purported error in omitting the appeal rights as an asset, because “vindication of the rule of law” is not a basis for Article III standing, nor is Schier’s “psychic satisfaction” from enforcement of the law.98

The Facts Claimed to Establish Standing are Not Set Forth in the Record

Standing to appeal creates a potential trap for the unwary. Appeals are typically decided on the factual record made before the trial court. But the appellant’s lack of standing to appeal may not come into focus until the appeal is well under way. Standing to appeal sometimes fails because the facts relied on to establish it are not in the record.

In Bender v. Williamsport Area School District,99 students contended that the school district violated the First Amendment by refusing to allow a student religious club to use school facilities on the same basis as other student clubs. The district court ruled in the students’ favor. The school district did not appeal, but one member of the school board (Youngman) did appeal. No one raised any question about his standing in the court of appeals, which ruled in his favor. After the Supreme Court granted the students’ petition for certiorari, it noticed that neither the school board nor any defendant besides Youngman opposed the students’ position, and only Youngman had appealed. The Supreme Court held that he lacked standing to appeal. He did not have standing to appeal in his capacity as a member of the school board, because he was only one member of the board, and the board, as a whole, had decided not to appeal.100 His alternate theory of standing contended that the judgment injured him in his personal capacity as parent of a child in the school. The Supreme Court rejected that argument, partly because the record did not contain evidence of that injury. As relevant here, it explained that the “presumption … is that the court below was without jurisdiction unless the contrary appears affirmatively from the record,” that the “factual predicate may not be gleaned from the briefs and arguments themselves,” and “[t]here is nothing in the record indicating anything about Mr. Youngman’s status as a parent” or that “he or his children have suffered any injury as a result of the District Court’s judgment, or as a result of the activities of [the club] since subsequent to the entry of that judgment.”101

D. Appeals Allowed Despite Superficial Absence of Standing

Even where these principles would normally require dismissal for lack of Article III standing, the Supreme Court, in some instances, allows appeals for policy reasons. These holdings apparently confirm at least the first part of Oliver Wendell Holmes’ famous observation that “[t]he life of the law has not been logic; it has been experience.”102

Appeal by Individual Plaintiff, Who Has Received All Possible Individual Relief, From Denial of Class Certification

In 1980, the Supreme Court held in Deposit Guaranty National Bank v. Roper103 that if class certification is denied and individual judgment is eventually entered in the plaintiff’s favor, the plaintiff can then appeal the denial of class certification in a post-judgment appeal. Roper held that the plaintiffs, despite having judgment in their favor for all the damages they could hope to obtain, had Article III standing to challenge denial of class certification because they had an economic interest in shifting part of their attorney fees to class members (which required class certification).104

Roper is limited to situations where the appellant asserts a continuing economic interest in shifting attorney fees and costs to others. Where the appellant asserts no such interest, Roper does not apply.105 The Supreme Court has also strongly suggested that Roper is unique to class actions. It likely does not apply even to the superficially similar issue of denial of collective-action status under the Fair Labor Standards Act.106

While Roper’s holding has diminished in importance given the subsequent enactment of Federal Rule of Civil Procedure 23(f) (authorizing courts to allow immediate appeal from denial of class certification), it creates an apparent inconsistency in Article III dogma. The usual rule is that Article III is not satisfied by the appellant’s interest in either recovering, or avoiding having to pay, attorney fees incurred in the litigation itself. The Roper opinion makes clear that the Court was animated largely by a desire to prevent defendants from “picking off” class representatives by offering the representatives full relief to moot their individual claims, denying them the injury needed to satisfy Article III on appeal and obtain class certification.107 The Court apparently seized on the only available injury to satisfy Article III. Regardless, Roper makes the appellant’s desire to shift attorney fees sufficient to satisfy Article III in the setting of denial of class certification, when it is insufficient elsewhere. The Supreme Court has noted, but not resolved, the inconsistency.108

Appellant Prevailed on the Judgment, But is Allowed to Appeal for Policy Reasons

Normally, a party that received an entirely favorable judgment cannot appeal to obtain review of an unfavorable determination, because of the statutory rule that a party must be aggrieved by the judgment.109 However, the Supreme Court has sometimes recognized exceptions to this rule when there is a “policy reason … of sufficient importance to allow an appeal” by the winner below.110

One example involves patent cases. When a patentholder sues a defendant for infringement, the defendant can defend on the grounds, among others, that it is not infringing the patent or that the patent is invalid. Suppose the trial court finds that the patent is valid but the defendant did not infringe it. Can the defendant appeal the conclusion that the patent is valid? Yes, but the scope of review depends on the procedural setting.

Electrical Fittings Corp. v. Thomas Betts Co.111 was a patent-infringement suit. The defendant raised an affirmative defense that the patent was invalid. The trial court held one claim of the patent to be valid, but not infringed. The successful defendant appealed, seeking reversal of the finding that the claim was valid. The court of appeals dismissed the appeal based on the rule that the prevailing party cannot appeal a judgment in its favor. The Supreme Court reversed. It held that the prevailing defendant could not force the appellate court to review the finding that the patent was valid, which did not affect the outcome as the defendant had not infringed the patent anyway. But, the Court held, the defendant was entitled to have the validity decision eliminated from the trial court’s judgment.112

As the Court later explained, in Electrical Fittings, “policy considerations permitted an appeal.”113 The finding that the patent was valid might scare other potential infringers into complying with the patent rather than challenging it, and there was a public interest in eliminating invalid patents.114 The dispute was not moot in the Article III sense, because the defendant still “alleged a stake in the outcome.”115 And when the defendant files a counterclaim seeking a declaratory judgment that the patent is invalid, that counterclaim provides a separate basis for jurisdiction, and the court has jurisdiction to entertain defendants appeal from the validity determination.116

Another policy-driven exception to the requirement that a prevailing party cannot appeal concerns civil-rights cases. A public official sued for damages for a civil-rights violation under 42 U.S.C. § 1983 can defend not only on the basis that his or her conduct did not violate the plaintiff’s constitutional rights, but also based on qualified immunity – that it was not clearly established that such conduct violated constitutional rights. Suppose an official is sued for a civil-rights violation, is found to have violated the plaintiff’s rights, but obtains a defense judgment based on qualified immunity. Can the official appeal to obtain review of the finding that he or she violated the plaintiff’s rights? The Supreme Court has held that at least the Supreme Court itself can review such an appeal, if the official regularly engages in such conduct as part of her job. In that event, the official retains the personal stake required by Article III and both she, the plaintiff, and the public all have an interest in resolving going forward whether the conduct violates the Constitution.117 An official who obtains a defense judgment in the trial court on the basis of qualified immunity can appeal to challenge the holding that her conduct violated the Constitution. Otherwise, the holding that such conduct violated the Constitution would affect the official’s and others’ conduct going forward, and there is a public interest in moving forward with such an appeal.118 The Court left open whether federal courts of appeals can review such appeals.119

The Electrical Fittings, Camreta and Roper exceptions are narrow. But, they are not necessarily exhaustive. A party that received an entirely favorable judgment in the trial court, but wants review of an unfavorable decision reached by the trial court, should consider whether the issue to be reviewed affects an important public interest going forward such that it should be resolved or the adverse finding, at least, eliminated. If so, and if the party has a continued personal stake required by Article III, there could be a policy-based reason for allowing it to appeal.

III. Conclusion

“Chance favors the prepared mind.”120 The lawyer who knows the standing requirements, and pauses to ask why the appellant has standing, will occasionally be rewarded with a silver bullet that stops the adversary’s appeal cold. Occasionally the careful lawyer may also discover a fatal defect in her own appeal, or even a way to cure the standing problem, before spending the client’s money on an appeal that will be dismissed. Either way, knowing the Article III standing requirements can give you an edge, or at least give you something to talk about at law-nerd conventions.

View Article

Greater specifics:

I have social security. Defendant constantly threatens social security

I have Medicare. Defendant constantly threatens Medicare.

I run a charity that serves the poor and immigrants. Defendant constantly threatens to cut funding to these NGOs, and has in fact, cut grants and programs to the indigent and to immigrant charity NGOs serving those groups.

I get food stamps. Defendant constantly threatens that and plans to cut food stamps are in the works

I am a voter. Trump constantly threatens voting rights and to disenfranchise millions of US citizens.

Sanctuary City. I have lived in Chicago for 30+ years since 1989 (except for 3 years in North Carolina). Defendant constantly threatens the rights of those that live in Sanctuary Cities and their funding.

Wrongful firings of govt lawyers that protect our rights. Defendant’s DOJ recently fired Maureen Comey, daughter of James Comey (who was previously fired for not pledging allegiance to Defendant). Maureen Comey had been prosecuting the Defendant in the Epstein case (his possible murder and disappearing client list)

Membership in organizations that protect immigrants, medicare, social security, food stamps, Sanctuary Cities, women’s rights (I am/was a member of NOW and Feminist Majority) and reproductive rights and rights to health care, access to Planned Parenthood which he constantly threatens. I still have 3 weeks to join some more of these to give me standing. Medicarerights.org looks good. I will like and follow to join (new web based forms of membership?) ACLU will join or at least like and follow on Instagram and FB NOW National Organization of Women. Like and follow Feminist Majority. Like and follow Planned Parenthood. Signed up to volunteer to help Planned Parenthood as a volunteer. Planned Parenthood is constantly under attack by Defendant and his thugs and goons and cronies.

I am a Medicare insurance recipient,

what Google AI says about Medicare status under Defendant’s present administration:

Based on the latest reports available from July 2025, there are several actions and proposals by the Trump administration that could be perceived as “cuts” or have a negative impact on Medicare, along with statements emphasizing protection of the program: Potential Medicare Cuts Triggered by Deficit: A budget reconciliation bill signed into law by President Trump in July 2025, while focused on various areas, including tax cuts, is projected to increase the deficit significantly. The Committee for a Responsible Federal Budget notes that this could trigger mandatory spending cuts to Medicare under the Statutory Pay-As-You-Go Act of 2010. The Medicare Rights Center estimates these cuts could total nearly $500 billion over the next decade, including a $45 billion reduction next year alone, unless Congress steps in to prevent them. Weakened Medicare Advantage Oversight: The Trump administration’s Centers for Medicare & Medicaid Services (CMS) issued a final rule for the 2026 Medicare Advantage (MA) program that reportedly omitted several consumer protections that were part of a previous proposed rule, according to the Center for Medicare Advocacy. Restricted Access to Care through Medicare Advantage: Project 2025, which aims to prepare for a second Trump term, proposes making Medicare Advantage (MA) the default enrollment option for all Medicare beneficiaries. The Center for American Progress warns that this could restrict older Americans’ access to care, limit choices, require prior authorization for services, and deny recommended care. They also estimate that a higher MA enrollment could lead to billions in overpayments to corporations at the expense of Medicare enrollees and taxpayers. Faster Clawback of Hospital Payments: The Trump administration plans to accelerate the clawback of $7.8 billion in Medicare payments to hospitals related to the 340B drug program. The American Hospital Association expressed concerns about this accelerated timeline and potential further cuts based on drug acquisition cost surveys. Executive Actions Impacting Drug Costs: The Trump administration rescinded an executive order designed to lower prescription drug costs for Medicare and Medicaid recipients, removing a $2 copayment cap on generic medications for Medicare beneficiaries and terminating a pilot program assisting states with expensive cell and gene therapies, according to Congressman Steve Cohen. However, The White House published a fact-check article stating that President Trump would always protect Social Security, Medicare, or Medicaid benefits, and that the administration would not cut these programs. They highlight President Trump’s repeated statements to that effect and emphasize the administration’s focus on eliminating fraud and waste in entitlement programs, citing estimates from the U.S. Government Accountability Office regarding improper payments in Medicare and Medicaid. It’s important to consider that the interpretations of these actions and proposals, and their potential impact, can differ depending on the perspective and priorities of different organizations and individuals.

Next Pasulka (Sex for Custody) Court Date: Wednesday, June 11, 2025 for Status

kenneth ditkowsky

3:35 PM (39 minutes ago)